One of the REITs I am looking to add on to my long-term investment portfolio is the blue-chip REIT Mapletree Logistics Trust (SGX:M44U) – for those of you who are interested in what’s in this personal long-term investment portfolio of mine, you can check it out here.

Before I begin to share the reasons why this logistics REIT is in my ‘shopping list’, let me first talk a little bit about the REIT (for the benefit of those who may be hearing about the REIT for the first time.)

Listed on the Singapore Exchange Securities Trading Limited in 2005, and eventually making its way as one of the constituents of Singapore’s benchmark Straits Times Index from 23 December 2019 (replacing Golden Agri-Resources), as at the end of the financial year 2019/20 (the REIT has a financial year-end every 31 March), its portfolio comprises a total of 145 logistics properties in the various geographical locations – 52 in Singapore, 9 in Hong Kong, 17 in Japan, 23 in China (where the REIT has a 50.0% interest in 15 properties), 10 in Australia, 13 in South Korea, 15 in Malaysia, and 6 in Vietnam.

In terms of revenue contribution from its tenants, as recorded in the REIT’s annual report for FY2019/20, other than CWT contributing 8.7% towards the REIT’s overall revenue (as such, should there be any non-renewals by the company, the REIT’s results may be negatively impacted in my opinion), Coles Group and Equinix each contributing 3.9% (towards the REIT’s overall revenue in FY2019/20), the remaining tenants contributed less than 2.0%.

Now that you have a better understanding of the logistics REIT, in the remainder of today’s post, you will learn about its financial performance, debt and portfolio occupancy profile, along with its distribution payout to unitholders over a 9-year period (between FY2011/12 and FY2019/20.) On top of that, you will also find the REIT’s most recent first quarter results of the financial year 2020/21 (ended 30 June 2020) compared to the previous financial year.

Let’s get started…

Mapletree Logistics Trust’s Financial Performance between FY2011/12 and FY2019/20

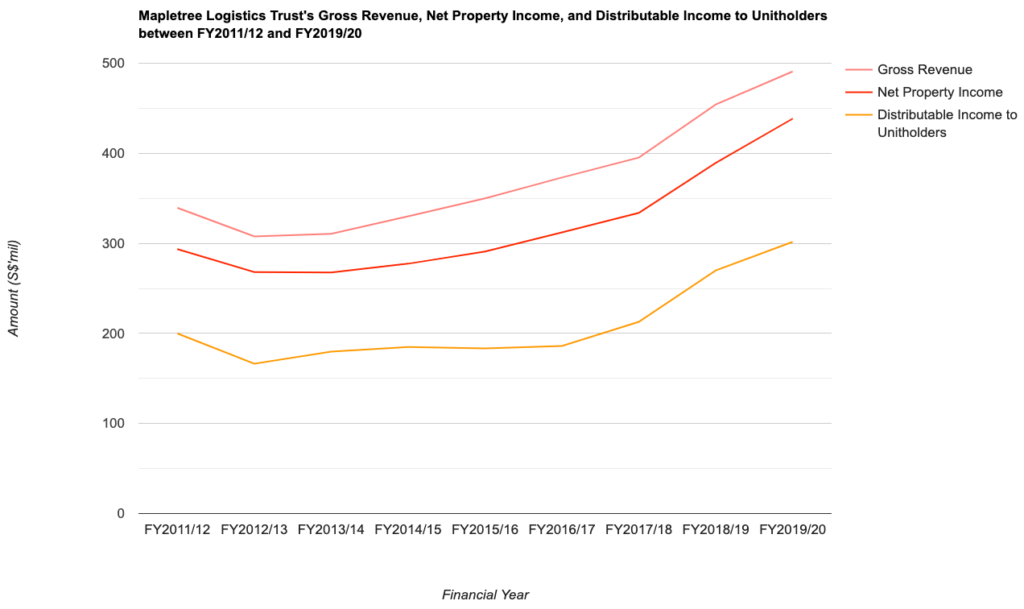

In this section, you will find the logistics REIT’s gross revenue, net property income, and distributable income to unitholders recorded over the past 9 financial years between FY2011/12 and FY2019/20:

| Financial Year | FY 2011/12 | FY 2012/13 | FY 2013/14 | FY 2014/15 | FY 2015/16 |

| Gross Revenue (S$’mil) | $339.5m | $307.8m | $310.7m | $330.1m | $349.9m |

| Net Property Income (S$’mil) | $293.6m | $268.1m | $267.6m | $277.4m | $290.9m |

| Distributable Income to Unitholders (S$’mil) | $199.9m | $166.4m | $179.7m | $184.9m | $183.3m |

| Financial Year | FY 2016/17 | FY 2017/18 | FY 2018/19 | FY 2019/20 | |

| Gross Revenue (S$’mil) | $373.1m | $395.2m | $454.3m | $490.8m | |

| Net Property Income (S$’mil) | $312.2m | $333.8m | $389.5m | $438.5m | |

| Distributable Income to Unitholders (S$’mil) | $186.1m | $212.9m | $270.0m | $301.7m |

Gross revenue saw year-on-year (y-o-y) improvements every single financial year since FY2011/12, with the exception of FY2012/13, due to the fact that the previous financial year results (i.e. FY2011/12) comprised of a 15-month period due to a change in financial year-end from 31 December to 31 March. Over a 9 year period, the REIT’s gross revenue grew at a compound annual growth rate (CAGR) of 4.2%.

The REIT’s net property income saw growths in 7 out of 9 financial years I have looked at. Y-o-y declines were seen in FY2012/13 (due to the previous financial year 2011/12 comprising of results for 15 months), and in FY2013/14 (due to a weaker Japanese Yen.) Over a 9-year period, its net property income grew at a CAGR of 4.6%.

Finally, its distributable income to unitholders also saw improvements every single financial year, except for in FY2012/13, as well as in FY2015/16 (as a result of a lack of one-off divestment gain distributed in the previous financial year 2014/15, and an enlarged unit base due to the REIT implementing the Distribution Reinvestment Plan.) That said, over a 9-year period, its distributable income to unitholders managed to grow at a CAGR of 4.7%.

The REIT’s resiliency in terms of its top- and bottom-line results is one of the reasons why it is in my ‘shopping list.’

Mapletree Logistics Trust’s Portfolio Occupancy Profile between FY2011/12 and FY2019/20

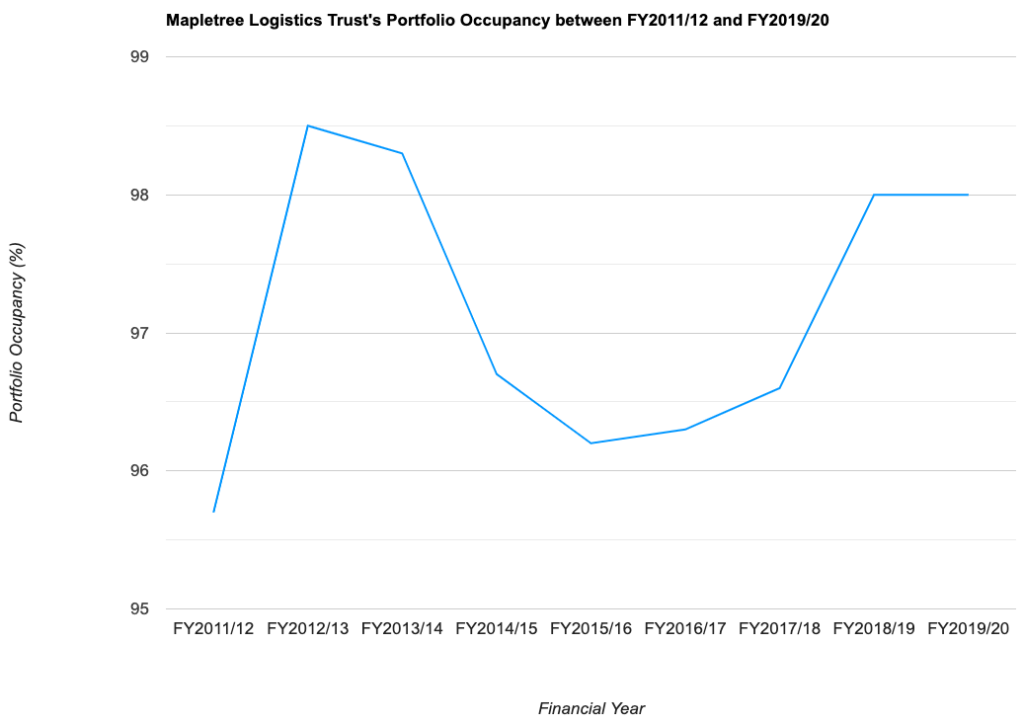

Moving on, let us take a look at the logistics REIT’s portfolio occupancy rate, along with its portfolio weighted average lease expiry (or WALE in short) by net lettable area:

| Financial Year | FY 2011/12 | FY 2012/13 | FY 2013/14 | FY 2014/15 | FY 2015/16 |

| Portfolio Occupancy (%) | 95.7% | 98.5% | 98.3% | 96.7% | 96.2% |

| Portfolio WALE (years) | 6.0 years | 5.3 years | 4.8 years | 4.3 years | 4.5 years |

| Financial Year | FY 2016/17 | FY 2017/18 | FY 2018/19 | FY 2019/20 | |

| Portfolio Occupancy (%) | 96.3% | 96.6% | 98.0% | 98.0% | |

| Portfolio WALE (years) | 4.0 years | 3.5 years | 3.8 years | 4.3 years |

One thing I like about the REIT is that, over the years, its portfolio occupancy have remained resilient – where its overall portfolio occupancy rate has been maintained at above 95.0%.

Debt Profile of Mapletree Logistics Trust between FY2011/12 and FY2019/20

Another aspect I look at is the REIT’s debt profile – my preference is towards one that has a gearing ratio a distance away from the regulatory level of 50.0% (this allows them sufficient debt headroom to make further yield-accretive acquisitions as and when the opportunity to do so arises), one where its interest coverage ratio is above 5.0x, as well as one that does not have an overly high cost of debt.

With that, let us take a look at Mapletree Logistics Trust’s debt profile over the last 9 financial years – between FY2011/12 and FY2019/20:

| Financial Year | FY 2011/12 | FY 2012/13 | FY 2013/14 | FY 2014/15 | FY 2015/16 |

| Gearing Ratio (%) | 35.2% | 34.1% | 33.3% | 34.3% | 39.6% |

| Interest Cover Ratio (times) | 6.0x | 6.6x | 8.7x | 7.5x | 5.9x |

| Average Term to Debt Maturity (years) | 4.2 years | 3.9 years | 3.6 years | 3.6 years | 3.5 years |

| Average Cost of Debt (%) | 2.3% | 2.4% | 1.9% | 2.1% | 2.3% |

| Financial Year | FY 2016/17 | FY 2017/18 | FY 2018/19 | FY 2019/20 | |

| Gearing Ratio (%) | 38.5% | 37.7% | 37.7% | 39.3% | |

| Interest Cover Ratio (times) | 5.6x | 5.6x | 4.9x | 4.9x | |

| Average Term to Debt Maturity (years) | 3.9 years | 4.5 years | 4.1 years | 4.1 years | |

| Average Cost of Debt (%) | 2.3% | 2.4% | 2.7% | 2.5% |

My Observations:

- Over the years, Mapletree Logistics Trust have been keeping its gearing ratio at under 40.0%, which is a safe distance from the 50.0% regulatory limit.

- In terms of its cost of debt over the past 9 financial years, it has largely remained stable.

- If there’s one thing I like to point out about the REIT’s debt profile over the years, it will be its interest cover ratio – where it has been declining over the years, from a high of 8.7x in FY2013/14 to 4.9x in FY2019/20.

Distribution Payouts to Unitholders of Mapletree Logistics Trust over a Period of 9 Financial Years

For those of you who are looking to invest in REITs that pays out unitholders on a quarterly basis, Mapletree Logistics Trust is one you may want to take a look at, as the management currently still declares a distribution payout to its unitholders on a quarterly basis.

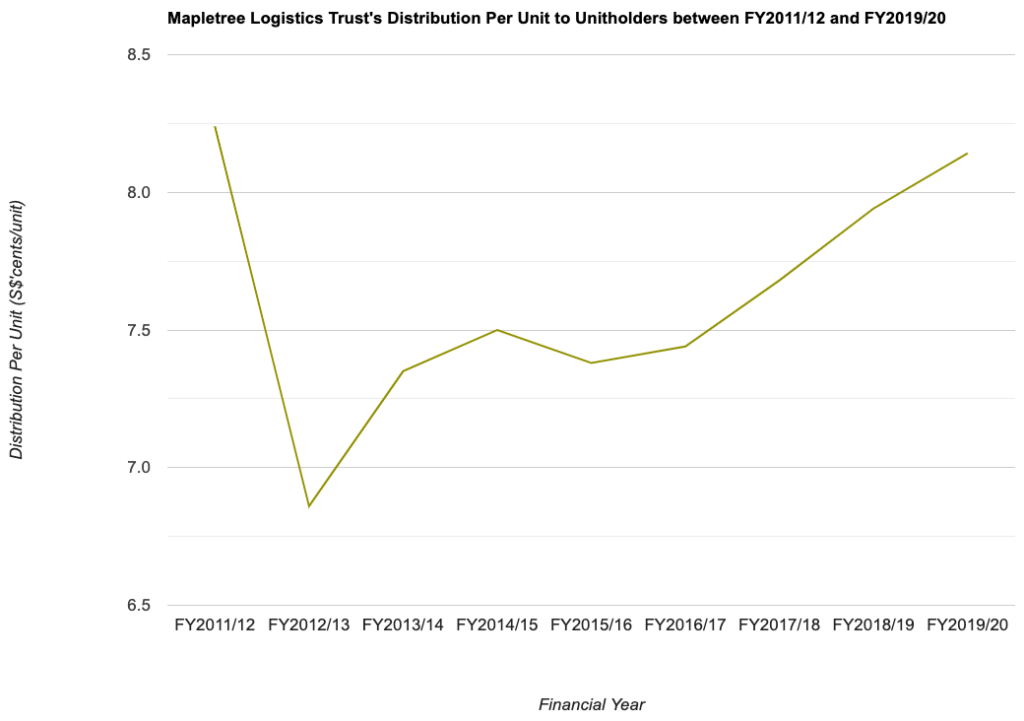

The following table is the logistics REIT’s distribution payout to its unitholders over the past 9 financial years (between FY2011/12 and FY2019/20):

| Financial Year | FY 2011/12 | FY 2012/13 | FY 2013/14 | FY 2014/15 | FY 2015/16 |

| Distribution Per Unit (S$’cents/unit) | 8.24 cents | 6.86 cents | 7.35 cents | 7.50 cents | 7.38 cents |

| Financial Year | FY 2016/17 | FY 2017/18 | FY 2018/19 | FY 2019/20 | |

| Distribution Per Unit (S$’cents/unit) | 7.44 cents | 7.68 cents | 7.941 cents | 8.142 cents |

Other than in FY2012/13 and FY2015/16, all the remaining 7 financial years saw Mapletree Logistics Trust increasing its distribution payout to unitholders – another thing about the REIT I desire.

Current Financial Year Performance of Mapletree Logistics Trust (Q1 FY2020/21) vs. the Previous Financial Year (Q1 FY2019/20)

As a result of the ongoing Covid-19 pandemic around the world, many companies saw their current financial year results weaken on a y-o-y basis. So, did Mapletree Logistics Trust’s latest quarter results (for Q1 FY2020/21 for the period between 01 April and 30 June 2020) suffer the same fate?

Let us take a look at some of the key statistics below:

| Q1 2019/20 | Q1 2020/21 | % Variation | |

| Financial Performance: | |||

| – Gross Revenue (S$’mil) | $119.8m | $132.4m | +10.5% |

| – Net Property Income (S$’mil) | $106.1m | $118.8m | +12.0% |

| – Distributable Income to Unitholders (S$’mil) | $73.6m | $77.8m | +5.7% |

| – Distribution Per Unit (S$’cents/unit) | 2.025 cents | 2.045 cents | +1.0% |

| Portfolio Occupancy Profile: | |||

| – Portfolio Occupancy (%) | 97.6% | 97.2% | – |

| – Portfolio WALE (years) | 4.8 years | 4.3 years | – |

| Debt Profile | |||

| – Gearing Ratio (%) | 36.8% | 39.6% | – |

| – Interest Cover Ratio (times) | 4.9x | 4.8x | – |

| – Average Term to Debt Maturity (years) | 3.8 years | 4.0 years | – |

| – Average Cost of Debt (%) | 2.8% | 2.3% | – |

The following are some of the positives and negatives to note regarding its latest quarter’s results:

Positives:

- Improvements in its gross revenue (due to higher revenue from its existing properties and contributions from accretive acquisitions in FY2019/20), net property income (due to lower utilities cost, maintenance costs, and absence of expenses related to the properties divested last financial year), and distributable income to unitholders.

- Continued growth in its distribution payouts (it saw a 1.0% y-o-y improvement to 2.045 cents/unit for the current quarter under review.)

- Its average cost of debt have come down by 0.5 percentage points compared to last year (to 2.3%)

Negatives:

- The REIT’s overall portfolio occupancy rate saw a slight 0.4 percentage point dip on a y-o-y basis.

- Its gearing ratio went up by 2.8 percentage points on a y-o-y basis to 39.6% (however, do take note that from its Q1 FY2020/21 results update, only 4% of its total debt is set to expire in the current financial year.)

In Conclusion

I like the REIT’s resilience in its latest Q1 FY2020/21 results even in the midst of the Covid-19 pandemic (in my opinion, while there are some slight negatives, but its results on the whole is an impressive one – at least to me.)

Another main reason why the REIT is in my ‘shopping list’ is because of its ability to record gradual growth in its top- and bottom-line over the years. The same goes for its steadily rising distribution payout to its unitholders.

Despite having said that, everything you have just read in this post is solely for educational purposes only. They are by no means a recommendation to buy or sell units of Mapletree Logistics Trust. Please do your own due diligence before you make any investment decisions.

Disclaimer: At the time of writing, I am not a unitholder of Mapletree Logistics Trust.

Stop Spending Hours Reading REIT Reports Every Quarter!

What if you could assess a REIT's portfolio occupancy, debt profile, valuation, and overall health in less than 30 seconds - without having to comb through a single quarterly report?

That's the problem the REIT Screener was built to solve.

Developed through a collaboration between ShareInvestor and The Singaporean Investor, the REIT Screener consolidates many of the key metrics and indicators I personally use when analysing REITs into one easy-to-use platform. Instead of spending hours extracting data manually every earnings season, you can now monitor the REITs you own and research new opportunities in just a few clicks.

If you're serious about REIT investing but don't have the time to manually track quarterly developments, the REIT Screener could be the shortcut you've been looking for:

Take a closer look at the REIT Screener here...

Comments (7)