Happy New Year to all my readers!

Apologies for the lack of update since the turn of the year as I was busy with some backend work to prepare for the upcoming earnings season, and also busy handling a series of bad events (including an accident involving my vehicle and another at a traffic light junction on Sunday, with my vehicle is the one being knocked onto, as well as my personal Facebook account being hacked 2 days later and I was being locked out of it – I’m still trying to explore various means to get in touch with someone in Facebook to explain my situation; if you happen to know someone there, or this happened to you before and you somehow manage to get your account unblocked, appreciate it if you can share with me here.)

Today, I’d like to share researches that I have done on a company by the name of PetroChina Company Limited (in Chinese, the company is known as ‘中国石油天然气股份有限公司’) – it is listed on the NYSE as an ADR since 06 April 2020 (under the ticker symbol NYSE:PTR), Stock Exchange of Hong Kong since 07 April 2020 (SEHK:0857), and also on Shanghai Stock Exchange (SHA:601857).

PetroChina Company Limited was formed as part of the restructuring of China National Petroleum Corporation (CNPC) back in 05 November 1999, and currently, it is the largest oil and gas producer and seller in the People’s Republic of China, as well as being one of the largest oil companies in the world – in fact, it has a business presence in Singapore, in that it operates the SPC (Singapore Petroleum Company) petrol stations (at the time of writing, they are the 3rd largest petrol station in the country, with over 40 service stations.)

So, is the US, Hong Kong, and China-listed company worthy of a ‘place’ in your long-term investment portfolio? The best way to answer this question (at least in my personal opinion) is to have a look at its historical performance – and in this post, you’ll read about PetroChina Company Limited’s financial results, debt profile, and dividend payouts over the past 5 years (between FY2017 and FY2021 – the company has a financial year ending every 31 December), and well as whether its current traded price is considered ‘cheap’ or ‘expensive’.

Let’s begin:

Financial Performance

I will be taking a look at several key figures – total revenue, net profit, net profit margin, and also return on equity recorded between FY2017 and FY2021 – a period of 5 years:

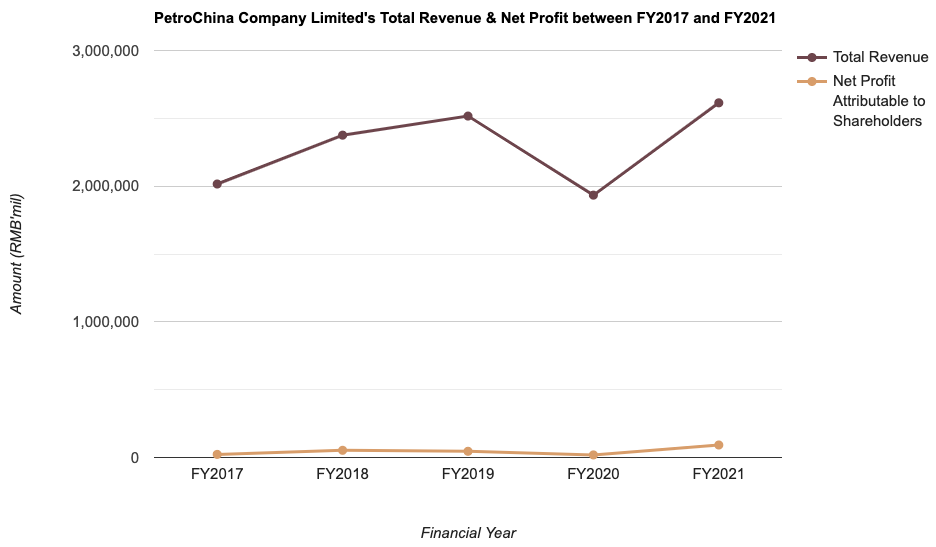

Total Revenue & Net Profit (RMB’mil):

| FY2017 | FY2018 | FY2019 | FY2020 | FY2021 | |

| Total Revenue (RMB’mil) | RMB 2,015,890m | RMB 2,375,934m | RMB 2,516,810m | RMB 1,933,836m | RMB 2,614,349m |

| Net Profit (RMB’mil) | RMB 22,798m | RMB 53,036m | RMB 45,682m | RMB 19,006m | RMB 92,170m |

My Observations: In terms of the company’s total revenue growth, the only year it saw year-on-year (y-o-y) decline was in FY2020, due to the decrease in sales volume and sharp decrease in selling prices of the majority of oil and gas products of the Group. Over a 5-year period, it grew at a compound annual growth rate of 5.3% – a stable growth in my personal opinion.

Its net profit fell in FY2019 (due to increase in expenses for purchasing oil and gas products, increase in employee renumeration and contribution to social security fund, increase in exploration expenses as a result of a rise in exploration efforts, increase in taxes, increase in net interest expenses, and finally, a huge decline in net exchange gain due to the impact of changes in exchange rate of USD against the RMB), as well as in FY2020 (as a result of a decrease in sales volume and sharp decrease in selling prices of the majority of oil and gas products of the Group.) Despite of that, its net profit managed to record a pretty impressive CAGR growth of 32.2% (largely contributed by a huge jump in its net profit in FY2021.)

Net Profit Margin (%):

| FY2017 | FY2018 | FY2019 | FY2020 | FY2021 | |

| Net Profit Margin (%) | 1.1% | 2.2% | 1.8% | 1.0% | 3.5% |

My Observations: The company’s net profit margin growth over the years have been inconsistent.

Return on Equity (%):

| FY2017 | FY2018 | FY2019 | FY2020 | FY2021 | |

| Return on Equity (%) | 1.9% | 4.4% | 3.7% | 1.6% | 7.3% |

My Observations: In layman terms, Return on Equity, or RoE for short, is a measure of profitability (in percentage terms) for every single dollar of shareholders’ money it uses in its business.

Just like the growth of its net profit margin, its RoE growth over the last 5 years have been inconsistent as well.

Debt Profile

Apart from its financial performance, another area I focus on (whenever I study about a company) is its debt profile – where my preference is towards those with minimal or no debt.

So, did PetroChina Company Limited’s debt profile over the last 5 years meet this requirement of mine? Let us find out in the table below:

| FY2017 | FY2018 | FY2019 | FY2020 | FY2021 | |

| Cash & Cash Equivalents (RMB’mil) | RMB 122,777m | RMB 85,954m | RMB 86,409m | RMB 118,631m | RMB 136,789m |

| Total Borrowings (RMB’mil) | RMB 465,275m | RMB 414,572m | RMB 466,722m | RMB 368,921m | RMB 340,450m |

| Net Cash/ Debt (RMB’mil) | RMB -342,498m | RMB -328,618m | RMB -380,313m | RMB -250,290m | RMB -203,621m |

My Observations: No doubt the company is in a net debt position throughout the entire 5-year period I have studied, but I noticed that between FY2019 and FY2021, its cash and cash equivalents have steadily increased, along with its total borrowings recording successive years of decline – this led to an improvement in the company’s net debt position. I will continue to keep a lookout on its debt profile in its results in the coming quarters.

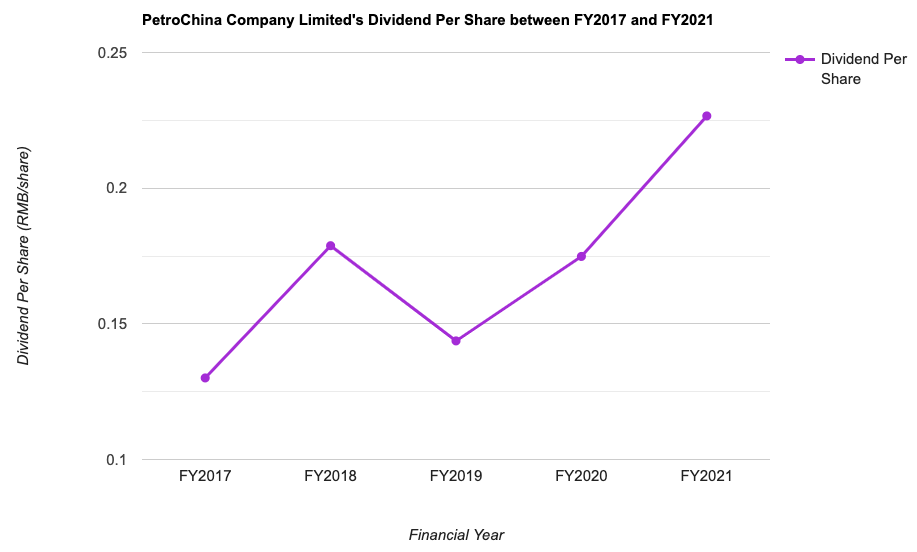

Dividend Payout to Shareholders

The management of PetroChina Company Limited declares a payout to its shareholders on a half-yearly basis – once when it releases its results for the first half of the financial year, and once when it releases its results for the second half.

The following table is the company’s dividend payout over the years (taken from AAstocks.com):

| FY2017 | FY2018 | FY2019 | FY2020 | FY2021 | |

| Dividend Per Share (RMB/share) | RMB 0.13006 | RMB 0.1788 | RMB 0.14371 | RMB 0.17484 | RMB 0.22662 |

My Observations: Apart from in FY2019, its dividend payout recorded y-o-y improvements in the other years. Over a 5-year period, it has grown at a CAGR of 11.8%, which, in my opinion, is still pretty decent.

Is the Current Share Price of PetroChina Company Limited Considered ‘Cheap’ or ‘Expensive’?

To find out whether the current price of a company is considered to be ‘cheap’ or ‘expensive’, I tend to compare its current valuations (based on its current traded price) against its average.

At the time of writing, PetroChina Company Limited is trading at HKD3.78 on the Hong Kong Exchange, and its current vs. its 5-year average valuations is as follows:

| Current | 5-Year Average | |

| P/E Ratio | 6.2 | 18.5 |

| P/B Ratio | 0.4 | 0.5 |

| Dividend Yield | 7.1% | 5.3% |

Looking at the table above, PetroChina Company Limited is currently trading at a ‘discount’ at the moment – due to its lower-than-average current P/E and P/B ratios, along with a higher-than-average dividend yield.

Closing Thoughts

Just like every company I have studied in the past, PetroChina Company Limited also have its fair share of pros and cons.

Some of the plus points include a steadily growing top-line (in total revenue), and also in its dividend payout to shareholders.

On the other hand, I note the irregular growth in its net profit margin and return on equity over the years, as well as the company being in a net debt position throughout the entire 5-year period (although it has seen gradual improvements in recent years.)

Finally, the company’s current traded price (at the time of writing of this post) is also deemed to be at a ‘discount.’

That said, I must say that the company’s industry is a cyclical one – with its financial results ver much depending on oil prices. Also, one thing to note is that, with countries in the world actively pursuing the sustainability agenda, and having a goal to achieve ‘Net Zero’, the use of such oil could gradually decline in the years to come, and as a result, the company’s financial performance could be impacted down the road.

With that, I have come to the end of my share on PetroChina Company Limited today. As always, I sincerely hope you’ve found the contents presented useful, and do note that all the opinions are solely mine which I am sharing for educational purposes only. They certainly do not imply and buy or sell calls for the company’s shares. You are strongly recommended to do your own due diligence before you make any investment decisions.

Disclaimer: At the time of writing, I am not a shareholder of PetroChina Company Limited.

Are You Worried about Not Having Enough Money for Retirement?

You're not alone. According to the OCBC Financial Wellness Index, only 62% of people in their 20s and 56% of people in their 30s are confident that they will have enough money to retire.

But there is still time to take action. One way to ensure that you have a comfortable retirement is to invest in real estate investment trusts (REITs).

In 'Building Your REIT-irement Portfolio' which I've authored, you will learn everything you need to know to build a successful REIT investment portfolio, including a list of 9 things to look at to determine whether a REIT is worthy of your investment, 1 simple method to help you maximise your returns from your REIT investment, 4 signs of 'red flags' to look out for and what you can do as a shareholder, and more!

You can find out more about the book, and grab your copy (ebook or physical book) here...

Comments (0)