Those of you who use cylinder gas in your kitchen should be familiar with the company Union Gas Holdings Limited (SGX:1F2), as chances are the LPG (Liquified Petroleum Gas) tank at your home is from them (the LPG tank in my previous home is from Union as well) – in case you’re not aware, Union Gas Holdings currently have the largest delivery fleet with over 200 vehicles.

Apart from serving residential homes, Union Gas Holdings also supply these LPG cylinder gas tanks to hawker centres, coffee shops, eating houses, as well as to commercial central kitchens.

In terms of the company’s businesses, on top of its LNG business segment (besides their namesake brand of LNG, the brand ‘Sungas’ is also under them), it is also in the natural gas business (where it provides Compressed Natural Gas, or CNG, at its ‘Cnergy’ fuel station in 50 Old Toh Tuck Road, as well as producing, selling, and distributing compressed and piped natural gas to industrial customers), and in the diesel business (at its ‘Cnergy’ stations.)

So, why is the company in my investment ‘watchlist’? You will find reasons why, along with some of the risks the company may be faced with in time to come (my personal opinion) in the rest of this post:

Reason #1: Improved Set of Financial Results in the Last 3 Years Post-IPO

Union Gas Holdings Limited was listed on the Singapore Exchange since 21 July 2017.

As such, I have looked at the company’s full-year results post-IPO (between FY2018 and FY2020), and they have been on an upward moving trend, as follows:

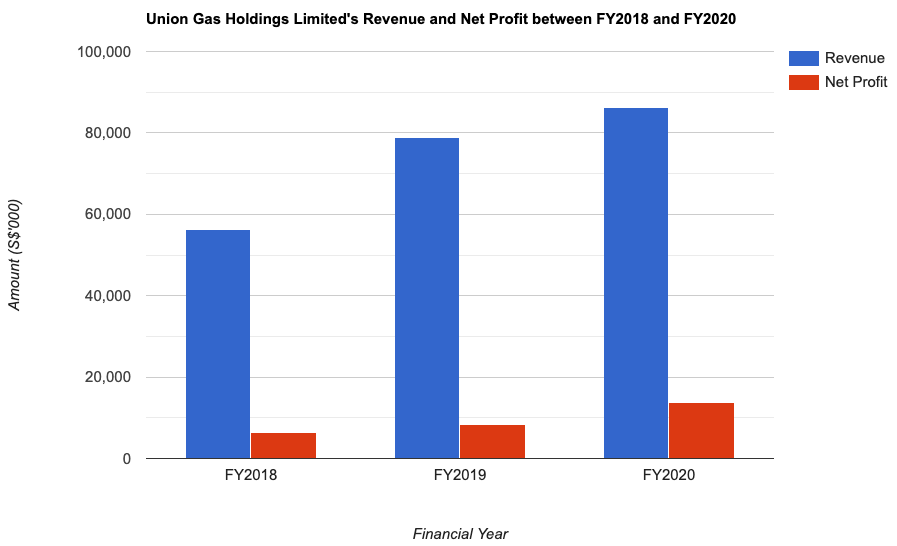

Revenue and Net Profit (S$’000):

| FY2018 | FY2019 | FY2020 | |

| Revenue (S$’000) | $56,361k | $78,801k | $86,190k |

| Net Profit (S$’000) | $6,424k | $8,417k | $13,864k |

Since post-IPO, its top- and bottom-line have recorded improvements every single year – of course, its latest full-year results is due to the ongoing Covid-19 pandemic, where most people stayed at home (especially during the 2-month circuit breaker between April and June) and cooked at home (and this contributed to an increase in revenue from its LPG business segment.)

Over a 3-year period, its revenue grew at a compound annual growth rate (or CAGR) of 15%, while its net profit by 29% – pretty impressive in my opinion.

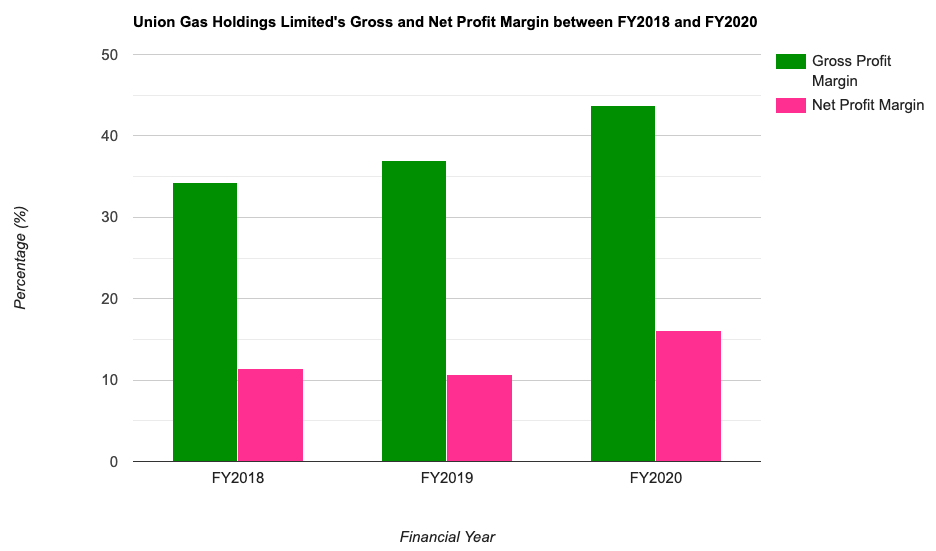

Gross and Net Profit Margin (%):

The following table is the company’s gross and net profit margins over the past 3 years which I have computed:

| FY2018 | FY2019 | FY2020 | |

| Gross Profit Margin (%) | 34.3% | 37.0% | 43.7% |

| Net Profit Margin (%) | 11.4% | 10.7% | 16.1% |

Equally impressive (in my opinion) is its gross profit margin, which have improved every year as well.

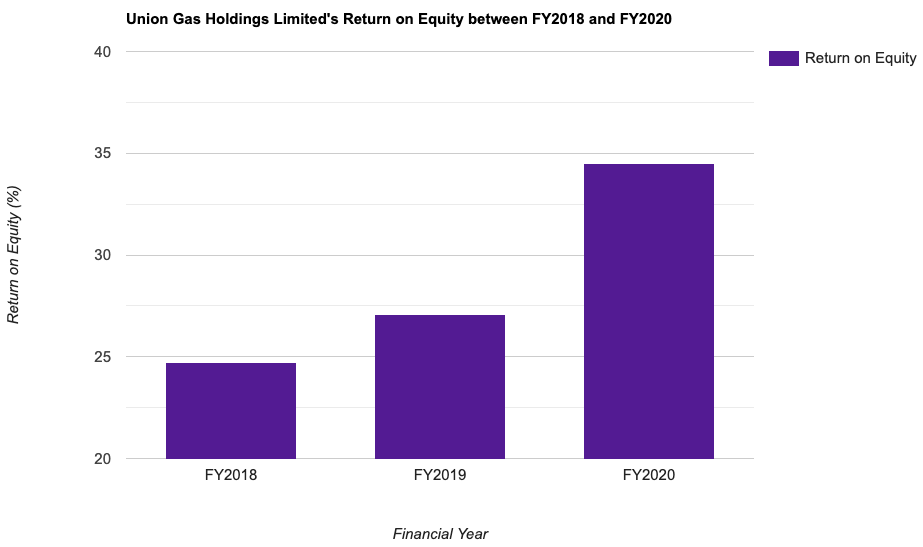

Return on Equity (%):

In layman terms, Return on Equity (or RoE) is a measure of the amount of profits a company is able to generate (in percentage terms) for every dollar of shareholders’ money it uses in its businesses. Ideally, my preference is towards companies that are able to maintain this ratio at above 15.0%.

The following table is the RoE of Union Gas Holdings I’ve computed:

| FY2018 | FY2019 | FY2020 | |

| Return on Equity (%) | 24.7% | 27.1% | 34.5% |

As you can see from the table above, not only has the company managed to maintain its RoE at above 15.0% in all the 3 years I have looked at, but it has been on an upward trend as well.

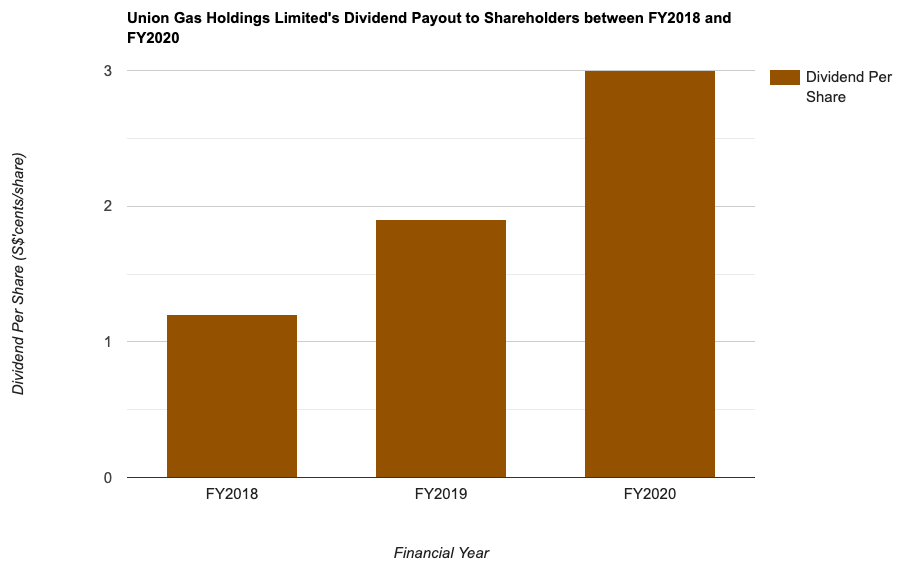

Reason #2: Increasing Dividend Payout Declared Every Single Year

One of the criteria I have when shortlisting companies to invest in is that the company must have the ability to declare a dividend payout (to its shareholders) on a regular basis (who doesn’t want to have some ‘pocket money’ coming into our bank accounts periodically?), and also its ability to increase its payout rates over time.

As far as Union Gas Holdings’ dividend payouts is concerned, apart from in FY2018, the company has been paying out a dividend to its shareholders on a half-yearly basis. Its payout since FY2018, along with its payout ratio, are as follows:

| FY2018 | FY2019 | FY2020 | |

| Dividend Per Share (S$’cents) | 1.2 cents | 1.9 cents | 3.0 cents |

| Dividend Payout Ratio (%) | 40.5% | 50.3% | 50.0% |

Union Gas Holdings have increased their dividend payout every single year since FY2018, with their payout ratio maintained at 50.0%.

At its current trading price of S$0.995 at the time of writing (at market close on Friday, 11 June 2021), this represents a yield of 3.0% based on its 3.0 cents/share of payout in FY2020.

Reason #3: Company is in a Net Cash Position

Another area I focus my attention on when studying a company is its debt profile – where my preference is towards those with minimal or no debt, and also one in a net cash position.

The following table illustrates Union Gas Holdings’ debt profile over the past 3 years (between FY2018 and FY2020):

| FY2018 | FY2019 | FY2020 | |

| Cash & Cash Equivalents as at the End of Period (S$’000) | $15,714k | $16,098k | $15,714k |

| Total Borrowings (S$’000) | $2,399k | $1,739k | $1,660k |

| Net Cash/ Debt (S$’000) | +$13,315k | +$14,359k | +$14,054k |

Two things about the company’s debt profile I like here – it being in a net cash position in all the 3 years I have looked at, as well as its total borrowing on a decline.

Key Risks of Union Gas Holdings (I have Identified)

There are two key risks I’ve identified when I was studying the company:

First, the company’s business operations are currently in Singapore only – as we are a small country, there is only so much room the company can grow. As such, it will come a time where its earnings will become stagnant.

Another area of concern is that, in terms of residential houses using LPG cylinder tanks, they are the older houses. That said, it will come a time (even though it will be decades down the road) where these houses will see their leases expire (at the end of 99 years) and they being torn down and rebuilt (with the new buildings using piped gas); as such, in the long run, we may see demand for these LPG cylinder gas going down (and this is likely to affect the company’s revenue.)

Closing Thoughts

To summarise, the company’s improving financial statistics, dividend payouts, as well as it being in a net cash position in all of the 3 years I have looked at are reasons why I’ve added the company into my investment ‘watchlist.’

On the other hand, however good the company’s number may be at this point in time, we cannot ignore the fact that growth potential of the company could be limited (as the company’s operations is only in Singapore), and that the demand for LPG cylinder gas tanks may decrease down the road (as the older houses that uses them gets demolished.)

With that, I have come to the end of my share of my analysis of Union Gas Holdings Limited. Do take note that everything you have just read above is purely for educational purposes only, and that they do not represent any buy or sell calls for the company’s shares. As always, please do your own due diligence before you make any investment decisions.

Disclaimer: At the time of writing, I am not a shareholder of Union Gas Holdings Limited.

Stop Spending Hours Reading REIT Reports Every Quarter!

What if you could assess a REIT's portfolio occupancy, debt profile, valuation, and overall health in less than 30 seconds - without having to comb through a single quarterly report?

That's the problem the REIT Screener was built to solve.

Developed through a collaboration between ShareInvestor and The Singaporean Investor, the REIT Screener consolidates many of the key metrics and indicators I personally use when analysing REITs into one easy-to-use platform. Instead of spending hours extracting data manually every earnings season, you can now monitor the REITs you own and research new opportunities in just a few clicks.

If you're serious about REIT investing but don't have the time to manually track quarterly developments, the REIT Screener could be the shortcut you've been looking for:

Take a closer look at the REIT Screener here...

Comments (2)