You may not heard of the NYSE-listed Restaurant Brands International Inc. (NYSE:QSR), but I am perfectly sure you have heard of the fast food brands ‘Burger King’ and ‘Popeyes.’ Together with ‘Tim Hortons’, these three brands come under the company.

Here are some quick information about each of the three brands under the company:

1. Burger King – Founded in 1954, it is currently the world’s second largest fast food hamburger restaurant; as at the end of FY2019 (ended 31 December 2019), the company owns or franchises a total of 18,838 Burger King outlets in more than 100 countries and US territories. You can browse through its website here – www.bk.com.

2. Popeyes – Founded in 1972, they are the world’s second largest quick service chicken concept, with a total of 3,316 outlets (either owned or franchised) as at the end of FY2019 – you can find out more here – www.popeyes.com.

3. Tim Hortons – This is probably the only brand under the company that we Singaporeans are not familiar with. Established since 1964, with a menu consisting of premium blend coffee, tea, espresso-based hot and cold specialty drinks, along with fresh baked goods, grilled Panini and classic sandwiches, wraps, soups, prepared food and other food products, there are currently 4,932 outlets (either owned or franchised) in North America and Canada – you can find out more in its website here – www.timhortons.com.

In the latest financial year ended 31 December 2019, Tim Hortons contributed a lion’s share towards the company’s total revenue (at US$3,344m or 59.7%), followed by Burger King (at US$1,777m or 31.7%), and then Popeyes (at US$482m or 8.6%.)

Now that you have a better understanding of Restaurant Brands International Inc.’s businesses, in the remainder of this post, let us take a look at its historical financial performance, debt profile, as well as its dividend payouts over the last 5 years (the period we will be look at is between FY2015 and FY2019), its current year results so far (i.e. 1H FY2020 ended 30 June 2020) compared against the previous year (i.e. 1H FY2019 ended 30 June 2019), and finally, whether or not the company’s current traded price is considered ‘cheap’ or ‘expensive’ based on its current vs. its historical valuations.

Let’s get started…

Historical Financial Performance of Restaurant Brands International Inc. between FY2015 and FY2019

Total Revenue and Net Profit (US$’mil):

| FY2015 | FY2016 | FY2017 | FY2018 | FY2019 | |

| Total Revenue (US$’mil) | $4,052m | $4,146m | $4,576m | $5,357m | $5,603m |

| Net Profit (US$’mil) | $104m | $346m | $626m | $612m | $643m |

Over a 5-year period, Restaurant Brand International’s total revenue recorded year-on-year (y-o-y) growths every single year – where it increased from US$4,052m in FY2015 to US$5,603m in FY2019, a compound annual growth rate (CAGR) or 6.7%.

Its net profit saw a y-o-y improvement in 4 out of 5 years I have looked at (the only exception is in FY2018), where over a 5-year period, it recorded an impressive CAGR of 44.0%!

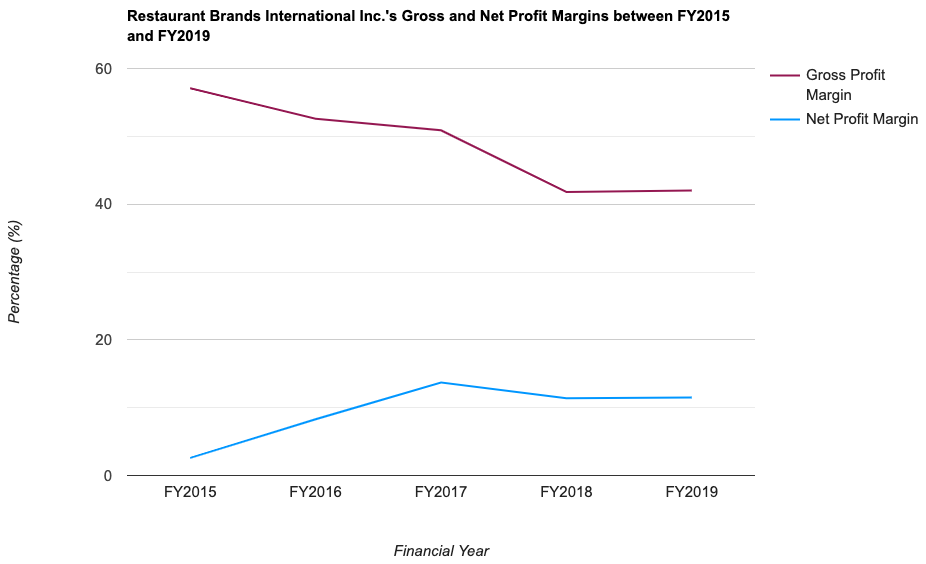

Gross and Net Profit Margins (%):

The following table is Restaurant Brands International’s gross and net profit margins I’ve computed:

| FY2015 | FY2016 | FY2017 | FY2018 | FY2019 | |

| Gross Profit Margin (%) | 57.1% | 52.6% | 50.9% | 41.8% | 42.0% |

| Net Profit Margin (%) | 2.6% | 8.3% | 13.7% | 11.4% | 11.5% |

One thing to take note of is that the company’s gross profit margin have declined over the years – where it went down from a high of 57.1% in FY2015 to a low of 41.8% in FY2018, before recording a small 0.2 percentage point improvement (to 42.0%) in FY2019.

As for its net profit margin, other than a spike up in FY2017 (to 13.7%), its growth over the years have more or less been at a steady pace.

Return on Equity (%):

In layman terms, Return on Equity, or RoE, expressed in percentage terms, is the amount of profit a company is able to generate for every dollar of shareholders’ money it uses in its businesses.

For instance, if a company has a RoE of 15.0%, it means the company is able to generate a profit of $15 for every $100 of shareholders’ money it uses.

The following table is Restaurant Brands International’s RoE over the years which I have computed:

| FY2015 | FY2016 | FY2017 | FY2018 | FY2019 | |

| Return on Equity (%) | 7.8% | 20.3% | 28.1% | 38.0% | 25.8% |

Its return on equity have improved every single year except for in FY2019. Personally, if the drop is a one-off, I am not too concerned.

Restaurant Brands International’s Debt Profile between FY2015 and FY2019

Apart from its historical financial results, another aspect about a company I look at is its debt profile – particularly, my preference is towards companies with minimal or no debt, along with one that is in a net cash position, as well as one that is able to maintain its current ratio at above 1.0 (meaning it is able to meet its short-term debt obligations.)

So, did Restaurant Brands International’s debt profile fulfil these three criteria of mine? Let us take a look in the table below:

| FY2015 | FY2016 | FY2017 | FY2018 | FY2019 | |

| Cash & Cash Equivalents as at the End of Period (US$’mil) | $758m | $1,476m | $1,097m | $913m | $1,533m |

| Total Borrowings (US$’mil) | $8,721m | $8,722m | $12,123m | $12,140m | $12,148m |

| Net Cash/Debt (US$’mil) | -$7,963m | -$7,246m | -$11,026m | -$11,227m | -$10,615m |

| Current Ratio | 1.2 | 1.7 | 1.1 | 1.1 | 1.3 |

From the table above, the company has been in a net debt position in all of the 5 financial years I have looked at. Not only that, its total borrowings have been on a steady rise as well every single year.

The only thing is that its current ratio have been maintained at above 1.0 in all of the 5 years – suggesting that the company is able to fulfil its short-term debt obligations.

Dividend Payouts of Restaurant Brands International over a 5-year Period

The management of Restaurant Brands International declares a dividend payout for its shareholders on a quarterly basis. However, if you are a Singaporean investing in a US-listed company, you need to take note that all dividends received are subjected to a 30.0% withholding tax, which means the final amount you receive will be 30.0% less than what is declared.

With that, let us take a look at the dividend payouts announced by the company over the last 5 years (between FY2015 and FY2019), along with the dividend payout ratios:

| FY2015 | FY2016 | FY2017 | FY2018 | FY2019 | |

| Dividend Per Share (US$/share) | $0.49 | $0.66 | $1.05 | $1.85 | $2.02 |

| Dividend Payout Ratio (%) | 98.0% | 45.5% | 41.3% | 76.4% | 85.2% |

The company have been increasing its dividend payouts to its shareholders over the years, where it has gone up from US$0.49/share in FY2015 to US$2.02/share in FY2019 – an impressive CAGR of 32.7% over a 5-year period.

Restaurant Brand International’s 1H FY2020 Results Compared against 1H FY2019

In early August 2020, Restaurant Brands International reported its financial results for the first half of the financial year 2020 ended 30 June 2020.

Let us take a look at some of the financial statistics reported, compared against the statistics reported in the same period last year (i.e. 1H FY2019 ended 30 June 2020):

| 1H FY2019 | 1H FY2020 | % Variance | |

| Total Revenue (US$’mil) | $2,666m | $2,273m | -14.7% |

| Net Profit (US$’mil) | $277m | $250m | -9.7% |

| Gross Profit Margin (%) | 42.3% | 43.9% | – |

| Net Profit Margin (%) | 10.4% | 11.0% | – |

| Cash & Cash Equivalents as at the End of Period (US$’mil) | $1,028m | $1,540m | +49.8% |

| Total Borrowings (US$’mil) | $12,113m | $12,715m | +5.0% |

| Net Cash/Debt (US$’mil) | -$11,085m | -$11,175m | – |

| Dividend Per Share (US$/share) | $1.00 | $1.04 | +4.0% |

In terms of its total revenue and net profit, both of them saw a y-o-y decline due to the temporary closure of its outlets relating to the ongoing Covid-19 pandemic. Also, on a y-o-y basis, sales growth in Tim Hortons and Burger King also weakened, while the sales of Popeyes in US and in its global outlets improved.

At the same time, compared to last year, its total borrowings continued to go up, and as a result, the company sank deeper into a net debt position as at the end of the first half of FY2020.

On the flip side, both the company’s gross and net profit margins recorded slight improvements compared to last year. Its dividend per share also saw a 4.0% y-o-y improvement as well to US$1.04/share.

Looking at its results for the second half of FY2020 ahead, due to the numbers of Covid-19 still on the rise, any lockdowns by governments in countries that Restaurant Brands International have operations in may negatively impact their sales growth.

As such, I am of the opinion that on a full-year basis, the company’s results (its total revenue and net profit) will be a weaker one compared to last year.

Is Restaurant Brands International’s Current Traded Price Considered ‘Cheap’ or ‘Expensive’?

If you have been following my company writeups, you will know that I will compare a company’s current valuations (based on its current share price) against its average over the years to determine whether or not its current traded price is considered ‘cheap’ or ‘expensive.’

As at the end of trading day in the US on 13 October 2020, the share price of Restaurant Brands International is at US$59.05. Based on this share price, its valuations is as follows:

P/E ratio: 22.9

P/B ratio: 5.8

Dividend Yield: 3.4% (calculated based on its dividend payout of US$2.02/share in FY2019)

The following table contains the valuations of Restaurant Brands International over the past 5 years, along with the average I’ve computed:

| FY2015 | FY2016 | FY2017 | FY2018 | FY2019 | Average | |

| P/E Ratio | 74.7 | 32.9 | 24.2 | 21.6 | 26.9 | 36.1 |

| P/B Ratio | 6.3 | 6.6 | 6.7 | 8.2 | 7.6 | 7.1 |

| Dividend Yield | 1.3% | 1.4% | 1.7% | 3.5% | 3.2% | 2.2% |

Comparing its current valuations against its 5-year average, it seems that the current traded price of Restaurant Brands International is considered ‘cheap’, due to its lower-than-average current P/E and P/B ratios, along with its higher-than-average current dividend yield.

In Conclusion

The company’s strong revenue and net profit growth over the years was stopped right in its tracks by the ongoing Covid-19 pandemic (as temporary restaurant closures affected its revenue and net profit growth for 1H FY2020.) However, despite of that, the management of the company still declared a higher dividend payout to its shareholders compared to last year (where on a y-o-y basis, its total dividend payout was up by 4.0%.)

Personally, I am concerned about the steady increase in its total borrowings, and that the company have sank deeper into a net debt position over the years. Another thing I may have some concerns about is its declining gross profit margin (between FY2015 and FY2018) – I will continue to keep a close watch on its gross profit margin in the quarters ahead to see if it manages to bounce back up, or it continues to go on a decline.

With that, I have come to the end of my writeup today on Restaurant Brands International Inc. Do take note that everything you have just read above is purely for educational purposes only. They do not imply any buy or sell recommendations for the company’s shares. You should always do your own due diligence before you make any investment decisions.

Disclaimer: At the time of writing, I am not a shareholder of Restaurant Brands International Inc.

Are You Worried about Not Having Enough Money for Retirement?

You're not alone. According to the OCBC Financial Wellness Index, only 62% of people in their 20s and 56% of people in their 30s are confident that they will have enough money to retire.

But there is still time to take action. One way to ensure that you have a comfortable retirement is to invest in real estate investment trusts (REITs).

In 'Building Your REIT-irement Portfolio' which I've authored, you will learn everything you need to know to build a successful REIT investment portfolio, including a list of 9 things to look at to determine whether a REIT is worthy of your investment, 1 simple method to help you maximise your returns from your REIT investment, 4 signs of 'red flags' to look out for and what you can do as a shareholder, and more!

You can find out more about the book, and grab your copy (ebook or physical book) here...

Comments (0)