Mapletree North Asia Commercial Trust (SGX:RW0U), with retail and office properties in Hong Kong, China, and Japan, is a REIT in my long-term investment portfolio (you can check out my entire long-term investment portfolio here.) It has released its annual report for FY2019/20 (which ended on 31 March 2020), along with its notice of AGM, last week.

As a unitholder of the REIT, I have gone through its latest annual report, took notes of the most important pointers, and am sharing them in this post (for the benefit of unitholders who had no time to go through the report):

Key Highlights of FY2019/20

Disruption of Operations in Festival Walk:

- The property’s retail shops was temporarily closed from 13 November 2019 to 15 January 2020, and its office tower was closed from 13 to 25 November 2019 as a result of damages caused by anti-government protestors in the country

- During the period of closure, no rental collection was made

- To mitigate the cashflow impact on the distributable income as a result of the temporary closure, and until the loss of revenue were recovered through insurance claims, the Manager have implemented distribution top-ups of S$32.9m for 3Q and 4Q of FY2019/20 to enable a certain level of distributable income to unitholders

- As far as insurance claims are concerned, based on my understanding in a note released by the REIT on 17 June 2020, the insurers have made an interim payment of HKD45m – approximately S$8m, as partial payment on the amount of the estimated claims relating to property damage – you can read the note in full here

Increasing Exposure to Japan with Acquisitions:

- The REIT increased their exposure to Japan by 16.8% (from 10.3%) with the acquisition of an 98.47% interest in 2 office buildings in Greater Tokyo, Japan in February 2020 – Omori Prime Building in Shingawa-ku, Tokyo, and mBAY POINT Makuhari in Mihama-Ku, Chiba, at at total amount of S$480m

Key Highlights from the REIT’s Letter to Unitholders

Update on Festival Walk:

- Apart from the temporary closure of Festival Walk due to damages by anti-government protestors in Hong Kong, retail tenants of the mall were also affected by the measures implemented by the Hong Kong government to contain the spread of Covid-19 in the country

- To support, as well as sustain the long-term relationship of tenants who were adversely affected by first the social unrests in Hong Kong, and subsequently Covid-19, rental reliefs amounting to S$18.1m were provided in FY2019/20. Rental reliefs were also extended through to 1Q FY2020/21, and the management shared that they will consider continuing with the relief measures as the impact of Covid-19 continues to evolve

In Terms of Financial Performance in FY2019/20:

- Gross revenue: Down 13.3% to S$354.5m (FY2018/19: S$408.7m), mainly due to rental reliefs granted to tenants of Festival Walk as a result of Covid-19 and social unrests prior to the mall’s temporary closure (for repair and restoration works)

- Net property income: Down 15.7% to S$277.5m (FY2018/19: S$329.0m)

- Distributable income: Down 5.3% to S$227.9m (FY2018/19: S$240.7m)

- Distribution payout: Down 7.4% to 7.124 cents (FY2018/19: 7.690 cents) due to lower income available for distribution, distribution top-ups, and an enlarged unit base (due to the issuance of Transaction Units to the Sponsor’s nominee, new units in respect of DRP, as well as payment of management fees to the Manager and Property Manager)

Property Operating Performance:

- Festival Walk (Office) – Fully occupied, with an average rental reversion of +6%

- Festival Walk (Mall) – 99.8% occupancy, with an average rental reversion of +8%; however, retail sales and footfall declined by 18.1% and 18.7% respectively due to social unrests and Covid-19

- Gateway Plaza – 91.5% occupancy, which is a decline from 99.0% recorded in the previous financial year due to a slowing economy and new supplies coming onstream

- Sandhill Plaza – 98.0% occupancy, with an average rental reversion of +10%

- Tokyo Properties – Collectively, their overall occupancy rate is at 99.1%; However, as one of the properties was converted from single to multi-tenancies upon expiry of the single tenancy, leases were renewed at lower rates to ramp up occupancy; for the two newly acquired office buildings in FY2019/20, the REIT will focus its efforts to increase occupancy and cost efficiencies to improve their net property income margin

Debt Profile:

- Aggregate leverage: 39.3% (FY2018/19: 36.6%) due to borrowings drawn to fund the acquisition of MBP and Omori

- Average term to debt maturity: 3.35 years (FY2018/19: 3.70 years)

- Effective interest rate: 2.43% per annum (FY2018/19: 2.47% per annum); 77% of the REIT’s interest cost has been hedged into fixed rates, and about 65% of expected foreign-sourced distribution income for 1H FY2020/21 has been hedged into SGD to mitigate exchange rate risk

- Approximately S$267m of debt is due for refinancing in FY2020/21, with no more than 25% of its total debt due in any financial years over the next 7 years

Management’s Outlook in the Financial Year Ahead:

- Festival Walk – Tough retail environment ahead will see vacancies to rise over the next 6-12 months along with lower renewal or re-let rental rates

- Gateway Plaza – Occupancy rates and rents likely to edge down due to reduced demand and new supply coming on stream in the Beijing office market

- Sandhill Plaza – Performance expected to remain resilient in the coming year, underpinned by tenants in the technology, media, and telecommunications sector, which are less affected by the current situation

- Japan Offices – With a nationwide state of emergency declared since mid-April 2020 and market uncertainties have led to slower leasing momentum in the office sector, with potential tenants adopting a “wait-and-see” attitude towards new commitments

- In light of the heightened uncertainties and headwinds, the REIT’s management is expecting the REIT’s performances in the year ahead (i.e. FY2020/21) to be weaker compared to FY2019/20

- REIT will also adopt half-yearly announcements of financial statements and half-yearly distributions with effect from FY2020/21

Gross Revenue Contribution by Assets (FY2018/19 vs. FY2019/20)

The following table highlights the REIT’s gross revenue contribution by their various assets:

| FY 2018/19 | FY 2019/20 | Difference (in percentage points) | |

| Festival Walk | 62.1% | 55.1% | -7.0pp |

| Gateway Plaza | 21.4% | 22.9% | +1.5pp |

| Sandhill Plaza | 6.1% | 7.1% | +1.0pp |

| Japan Properties | 10.4% | 14.9% | +4.5pp |

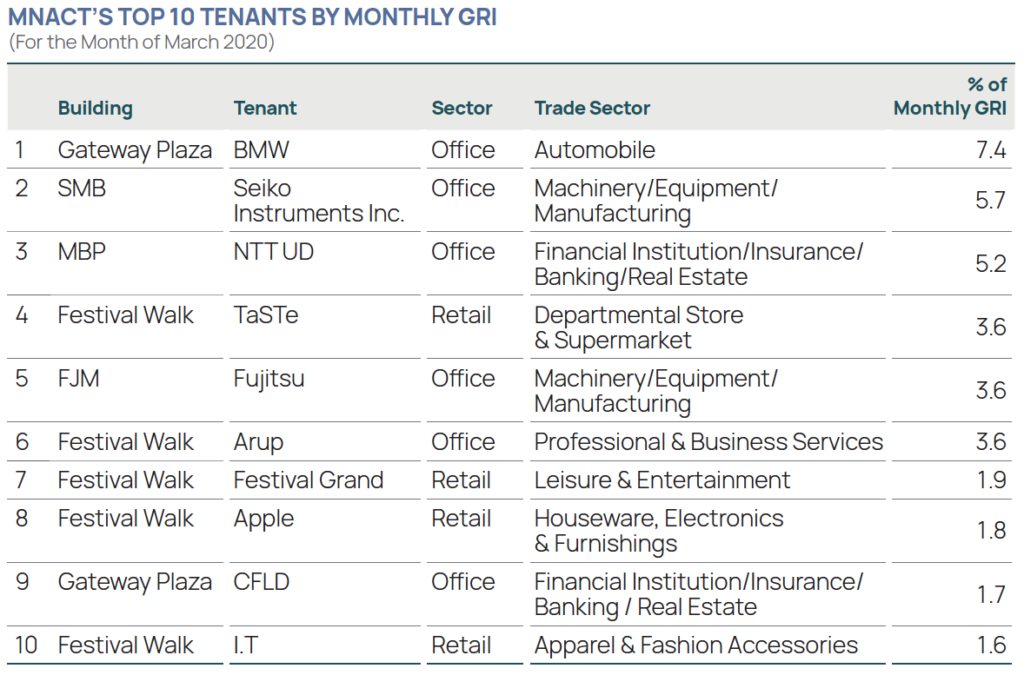

Top 10 Tenants of Mapletree North Asia Commercial Trust by Monthly Gross Rental Income

The following image (taken from the REIT’s annual report for FY2019/20) is the REIT’s top 10 tenants based on their monthly gross rental revenue contribution for the month of March 2020:

Details of the REIT’s 7th Annual General Meeting

- Date and Time: Thursday, 16 July 2020, at 2.30pm

- Registration Link: Here (Deadline for registration is on 13 July 2020 at 2.30pm, with confirmation link to be received by 15 July 2020 at 2.30pm)

- Question: Can be submitted when registering for the meeting, or via email to enquiries_mnact@mapletree.com.sg (please also submit your full name, full address, and the manner you hold your unitholders in the REIT, along with your questions)

In Conclusion

From what I have read in the REIT’s latest annual report, it seems that there are lots of headwinds in the financial year ahead. The management have also cautioned that the coming year’s performances will be a weaker one compared to the previous year – and that will likely mean a lower distribution per unit for us unitholders.

No doubt the REIT’s acquisition of the 2 Japan properties reduces its concentration on Festival Walk, but at the end of FY2019/20, it still contributes a lion’s share towards the REIT’s gross revenue (at around 55%.)

I have since since signed up to attend the REIT’s virtual AGM (details can be found above), along with submitting three questions which I hope the REIT can address:

- Are there any plans for the REIT to make any M&A activities this year to further reduce the concentration of revenue contribution on Festival Walk (which at the end of FY2019/20 was 55%), taking into considering the economic headwinds ahead (no thanks to Covid-19 pandemic.)

- Is there any chance that the REIT (MNACT) be merged into Mapletree Commercial Trust? I personally feel is a win in both ways – for MNACT, it solves the problem of gross revenue concentration on Festival Walk; for Mapletree Commercial Trust, it allows for geographical diversification. Also, an enlarged REIT will also result in more liquidity.

- Is there any timeline as to when the outcome of the insurance claim (for the damages in Festival Walk) be let known, and the case be finally closed?

I look forward to attending the REIT’s AGM in a few weeks time to receive the latest updates from the management.

Related Documents to Download

Disclaimer: At the time of writing, I am a unitholder of Mapletree North Asia Commercial Trust.

Are You Worried about Not Having Enough Money for Retirement?

You're not alone. According to the OCBC Financial Wellness Index, only 62% of people in their 20s and 56% of people in their 30s are confident that they will have enough money to retire.

But there is still time to take action. One way to ensure that you have a comfortable retirement is to invest in real estate investment trusts (REITs).

In 'Building Your REIT-irement Portfolio' which I've authored, you will learn everything you need to know to build a successful REIT investment portfolio, including a list of 9 things to look at to determine whether a REIT is worthy of your investment, 1 simple method to help you maximise your returns from your REIT investment, 4 signs of 'red flags' to look out for and what you can do as a shareholder, and more!

You can find out more about the book, and grab your copy (ebook or physical book) here...

Comments (0)