Now that we’re unable to dine in Haidilao’s (海底捞) chain of restaurants as dining in is still not permissible in Singapore, besides ordering takeaways, many also buying pre-packaged condiment bases, as well as sauces, to enjoy their favourite hotpot in the comfort of your own home with their loved ones.

As I’ve mentioned in the title of today’s writeup, these products are produced by a company by the name of Yihai International Holding Limited, which was listed on the Hong Kong Stock Exchange under the ticker SEHK:1579 since 13 July 2016.

In this post, I’ll be sharing with you all the researches I’ve done about the company – where you will learn more about the company’s operations (including other brands they have in the marketplace), three years of post-IPO financial results, debt profile, along with dividend payouts, and finally, I will be comparing the company’s current valuations (based on its current share price at the time of writing) against its 3 year average to find out whether or not it is current trading at a discount or at a premium.

Let’s begin…

A Brief Introduction about Yihai International Holding Limited

- Yihai International Holdings is the sole supplier of hotpot soup flavouring condiment, and sauces for Haidilao.

- The company has exclusive rights to use the “Haidilao” (海底捞) brand for their condiment products on a royalty-free basis for a perpetual term commencing from 01 January 2007.

- Other products by the company includes spicy stir-fry pot and pickles and fish stew condiments. A full catalogue of its products can be found here.

- Besides Haidilao Group, and its affiliates and their distributors, Yihai International also sell their products through the various e-commerce channels including Tmall and JD.com. The company also supplies condiment products to a number of third-party catering service providers and other customers.

- On top of that, the company have also started to export their products to overseas markets (including North America, Europe, as well as Asia) in 2015.

Historical Results between FY2017 and FY2019

Yihai International has a financial year end on 31 December. As the company is only listed on the HKEX on 13 July 2016, in this section, I will be reviewing the company’s full-year post-IPO historical results between FY2017 and FY2019 (a period of 3 financial years):

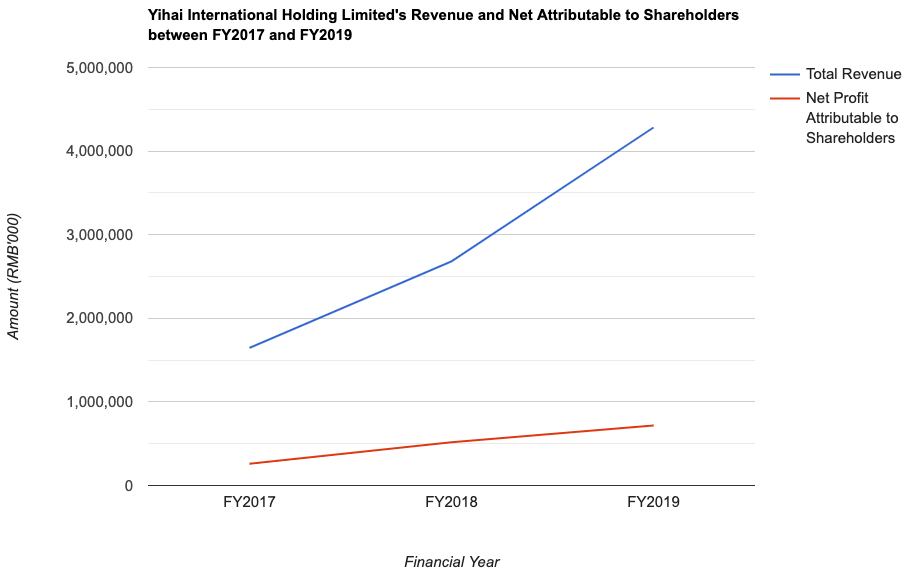

Revenue, and Net Profit Attributable to Shareholders:

| FY2017 | FY2018 | FY2019 | |

| Total Revenue (RMB’000) | RMB 1,646,221k | RMB 2,681,373k | RMB 4,282,488k |

| Net Profit Attributable to Shareholders (RMB’000) | RMB 260,670k | RMB 517,793k | RMB 718,634k |

Both the company’s top- and bottom-line growth in my opinion is impressive, where its revenue grew at a compound annual growth rate (or CAGR) of 37.5%, while its net profit attributable to shareholders saw a CAGR of 40.2%.

Gross Profit Margin, Net Profit Margin, and Return on Equity:

The following table is Yihai International’s gross profit margin, net profit margin, as well as return on equity which I have calculated:

| FY2017 | FY2018 | FY2019 | |

| Gross Profit Margin (%) | 37.2% | 38.7% | 38.3% |

| Net Profit Margin (%) | 15.8% | 19.3% | 16.8% |

| Return on Equity (%) | 17.4% | 25.8% | 27.5% |

The company’s gross and net profit margin have remained consistent over the years, and its return on equity have increased every year over the past 3 years – something which I am happy to see.

Current Ratio:

Another thing I look at when I study a company is whether or not it is able to fulfil its short-term (meaning under one year) obligations, and they way to find out is to calculate its “current ratio” (by dividing its current assets by its current liabilities.) If the company’s current ratio is under 1.0, it means that the company may have problems meeting its short-term obligations.

The following table is Yihai International’s current ratio which I’ve calculated:

| FY2017 | FY2018 | FY2019 | |

| Current Ratio | 5.0 | 4.5 | 4.2 |

While over the years, its current ratio have slipped from 5.0 in FY2017 to 4.2 in FY2019, its current ratio is at a very comfortable level.

Net Cash or Net Debt?

Yihai International does not have any borrowings in the three financial years I have looked at, so it is in a net cash position.

The following table is the company’s cash and cash equivalents at the end of the respective financial years:

| FY2017 | FY2018 | FY2019 | |

| Cash & Cash Equivalents as at the End of 31 December (RMB’000) | RMB 1,130,205k | RMB 1,179,910k | RMB 1,036,396k |

Yihai International’s Dividend Payouts to Shareholders over the Past 3 Financial Years

Yihai International pays out a dividend on an annual basis, and the ex-dividend date is usually around the end of May every year.

Let us take a look at the company’s dividend payout to shareholders, along with its payout ratio:

| FY2017 | FY2018 | FY2019 | |

| Dividend Per Share (HKD/share) | HKD0.06 | HKD0.16 | HKD0.23 |

| Dividend Payout Ratio (%) | 19.1% | 26.7% | 28.2% |

Over the past 3 years, its dividend payout to shareholders have been on a rise over the years – from 6.0 HK cents/share in FY2017 to 23.0 HK cents/share in FY2019, a CAGR of 55.8%.

In terms of its dividend payout ratio, you can see that the company have retained a huge portion of its earnings for its business growth.

Is Yihai International’s Current Share Price Considered Cheap/Expensive?

One of the ways I use to find out whether or not a company’s current share price is considered cheap or expensive is to take its current valuations (based on its current share price), and compare against the company’s historical valuations.

At the time of writing, the share price of Yihai International is trading at HKD71.35 and as such, its current valuations is as follows:

P/E ratio: 85.8

P/B ratio: 23.9

Dividend Yield: 0.3% (computed based on its dividend per share of 23.0 HK cents/share in FY2019)

The company’s 3-year average valuations (which I have calculated) is as follows:

P/E ratio: 36.7

P/B ratio: 9.8

Dividend Yield: 0.7%

When I compare the company’s current valuations against its 3-year average, at its current share price, Yihai International is concerned expensive, due to its higher-than-average current P/E and P/B ratios, along with its lower-than-average current dividend yield.

In Conclusion

Yihai International’s historical financial results over the past 3 years are certainly impressive – with year-on-year improvements seen every single year, as well as a CAGR of 37.5% for its revenue growth and a CAGR of 40.2% for its growth in the net profit attributable to shareholders.

I also like the company for the fact that it is debt-free, and that its dividends to shareholders have also grown every single year over the past three years.

Having said that, the company is not without risks – one key risk that comes to me is that, as the brands’ products are all under the “Haidilao” (海底捞) brand which they have the exclusive rights to use, should the brand end up not being able to maintain exclusive rights to continue to use the “Haidilao” (海底捞) brand, or that the brand name is negatively affected, its business will be adversely impacted as a result.

Another thing is the company’s current valuations, which in my opinion is a bit on the high side when compared against its 3-year average.

However, having said all of that, the above sharing is for educational purposes only, and it does not constitute any buy or sell calls for the company. Please do your own due diligence before you make any investment decisions.

Disclaimer: At the time of writing, I am not a shareholder of Yihai International Holdings Limited.

Are You Worried about Not Having Enough Money for Retirement?

You're not alone. According to the OCBC Financial Wellness Index, only 62% of people in their 20s and 56% of people in their 30s are confident that they will have enough money to retire.

But there is still time to take action. One way to ensure that you have a comfortable retirement is to invest in real estate investment trusts (REITs).

In 'Building Your REIT-irement Portfolio' which I've authored, you will learn everything you need to know to build a successful REIT investment portfolio, including a list of 9 things to look at to determine whether a REIT is worthy of your investment, 1 simple method to help you maximise your returns from your REIT investment, 4 signs of 'red flags' to look out for and what you can do as a shareholder, and more!

You can find out more about the book, and grab your copy (ebook or physical book) here...

Comments (2)